Fed 0.25 rate cut and it's mortgage impact

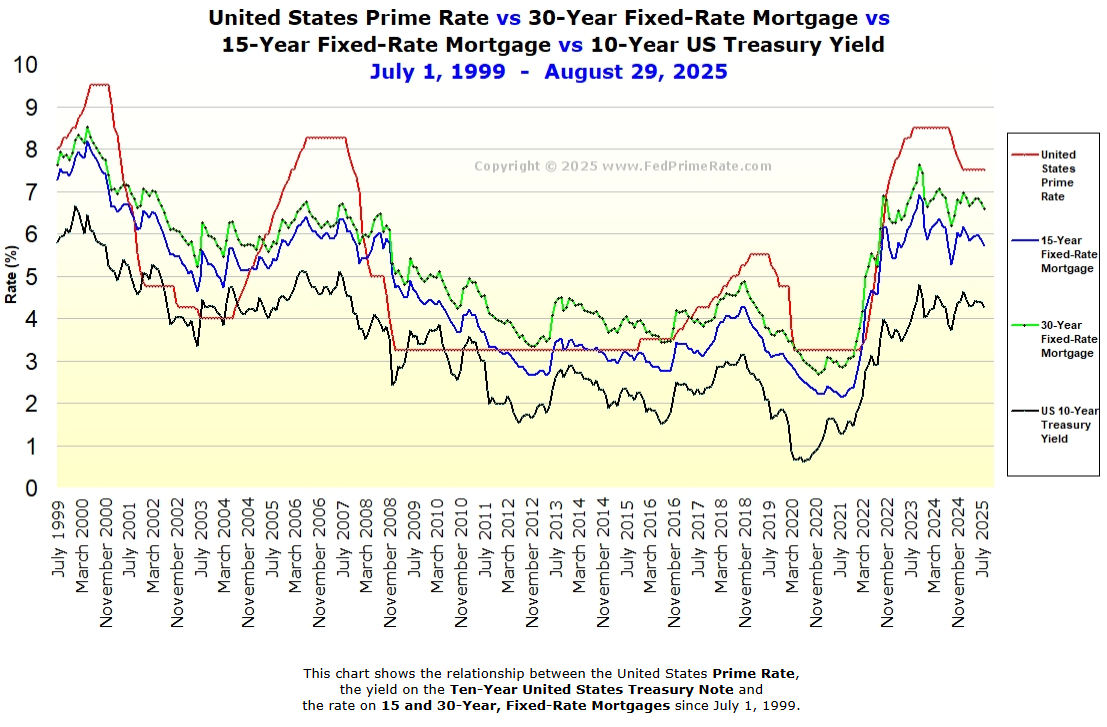

Chart Courtesy of FedPrimeRate.com

1. Fed’s New Rate Cut: What’s Happened?

On September 17, 2025, the Federal Reserve cut its target federal funds rate by 25 basis points, lowering it to a range of 4.00%–4.25% — the first rate cut since December 2022. The Fed cited weakening labor markets and elevated inflation as key reasons. Officials also signaled two more cuts may come before the end of the year. Investopedia+1

2. Why Mortgage Rates Don’t Immediately Drop

It’s tempting to assume that when the Fed cuts its rate, mortgage rates automatically fall—but that’s not how it works (usually):

Fed Funds Rate vs. Mortgage Rates

The federal funds rate is what banks charge each other overnight for loans. It influences short-term interest rates.

Fixed-rate mortgages (30-year, 15-year) are tied more closely to long-term bond yields, particularly the 10-year U.S. Treasury note. CBS News+1

Adjustable-rate mortgages (ARMs) may react more quickly to Fed moves, but even those depend on benchmarks like SOFR (Secured Overnight Financing Rate), not directly on Fed policy.

3. The 10-Year Treasury: The Real Anchor for Mortgage Rates

Mortgage rates typically follow the 10-year Treasury yield because:

Both are long-term instruments, with the 10-year Treasury serving as a benchmark for government borrowing.

Fixed mortgage rates usually include a spread over the 10-year yield to account for risk, lender costs, and mortgage-backed securities (MBS). Fannie Mae+1

When yields rise, mortgage rates tend to go up. When yields fall, mortgaged-backed rates often drop too—though not always perfectly. Kiplinger+1

4. What This Means After Today’s Fed Cut

Mortgage rates had already modestly declined ahead of the Fed move, driven by lower 10-year treasury yields. For example, 30-year fixed rates dropped to around 6.35%, while the 10-year yield fell to about 4.02%. Business Insider+1

Short-term relief: Expect some easing for ARMs and refinances, but fixed rates may not immediately detect a 0.25% Fed cut.

Forward guidance matters: The Fed signaling two more cuts this year can drive long-term expectations lower, which can influence bond investors and push 10-year rates (and mortgage rates) down over time.

5. Why Fed Cuts and Mortgage Rates Diverge

Even with Fed easing, fixed mortgage rates don’t necessarily fall the same amount:

The spread between mortgage rates and 10-year yields can widen or shrink based on:

Inflation expectations

Housing market demand

MBS supply and investor sentiment

Bank credit conditions and lender risk Appetite Brookings+1

When 10-year Treasury yields have dropped, but mortgage rates didn’t fall as much, it’s often because that spread stayed elevated due to these factors.

6. What Homebuyers & Homeowners Should Do

If you’re refinancing: The recent dip in long-term yields and Fed signaling may provide a small window to lock in lower rates.

If you’re buying: Don’t assume fixed rates will drop 0.25% just because the Fed cut. Monitor 10-year Treasury trends and lender spreads.

If you’re selling: Lower mortgage rates may eventually boost buyer demand—but timing can lag by weeks or months.

Final Takeaway

The Fed’s 0.25% rate cut is important for the economy—but it doesn’t translate directly into mortgage savings. Mortgage rates ride on long-term bond yields, especially the 10-year Treasury, and include risk-related spreads that can push them higher or lower.

Staying informed about both is key for making strategic moves in real estate—whether you’re buying, selling, or refinancing. Keep watching those Treasury yields.